Most people can be divided into two categories: More is more and less is more. I generally skew towards a simplified approach to life, so it might surprise you to know that when it comes to bank accounts, I’m a big fan of more. As you might expect, this is especially important for entrepreneurs.

Having multiple bank accounts can help you improve cash flow, and it can also help you get a better handle on your money. So just how many bank and/or investmene accounts should you have? I’m making the case for nine. Let’s dig in.

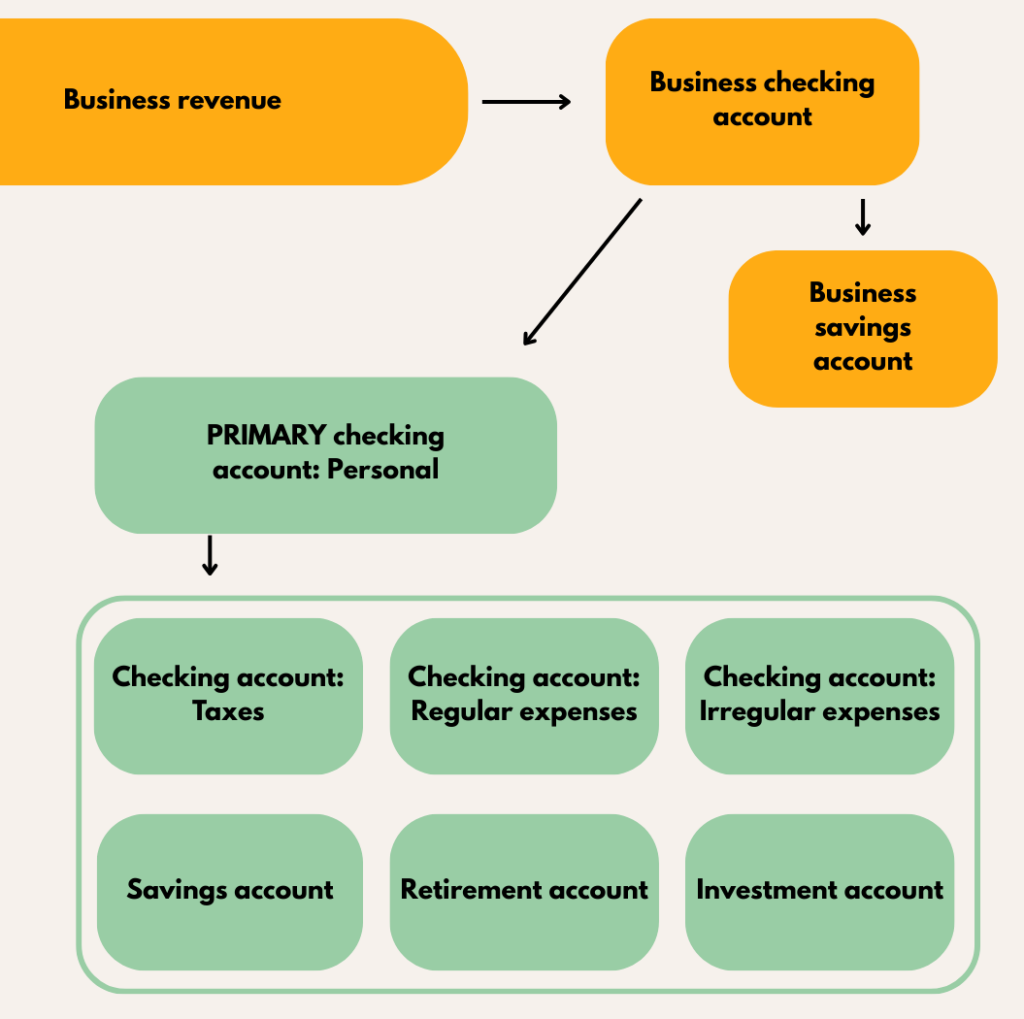

Separate business and personal

That’s a given. I don’t care how new your business is, or how you have it structured, as soon as you’re making money from something that could turn into a business, create a separate bank account for it. In fact, you should probably create two separate bank accounts: Checking and savings. Eventually, you may want even more accounts linked specifically to the business, but a checking and savings account are a good place to start.

Personal accounts

Any revenue from your business should go to your business checking account. From there, it can go either into the business savings account or to pay vendors, employees, and so on. Included in that? Paying you. At this point, the money moves to your personal checking account. But I don’t think you should have just one. Think of the personal checking account that you pay your salary (or profits) into as a hub. From here, flow your money into various individual accounts.

A tax account

How much money you flow into your tax account will depend on your personal circumstances and how you pay yourself. If you aren’t paying yourself as a W-2 employee, you’ll need to proactively withhold federal and state income taxes as well as Social Security and Medicare taxes (which are higher for a business owner, as you’re contributing both the employee and employer portion). Of course, I also recommend working with a tax specialist who can tell you how much to set aside for taxes. But regardless, automatically filter money earmarked for Uncle Sam into a separate tax account where you aren’t tempted to spend it.

A savings account

Think of this as your traditional savings account for emergencies and general cushioning. In business terms, this is your “cash reserve.” Keep it in a separate account so you can:

- Automate contributions so you start building your savings.

- Avoid temptation. Yes, you might still dip into these funds, but you’ll need to think twice before you do by default.

A retirement account

This isn’t a classic bank account, but it’s still a separate “designation” or account for your money. And you’ll still want to automate the money that flows here, so it gets its own account label. What type of account you have (and whether you have more than one!) will depend on your personal circumstances. A tax strategist and wealth advisor can help you build out this part of your financial plan on purpose.

So far we’ve prioritized paying yourself (and Uncle Sam) first. But most of us also have some pretty important expenses to pay each month, so that’s the next account.

Expense account

This account should be for your mandatory monthly expenses: rent or mortgage, utilities, car payments, a gym membership, whatever you pay each month. If you and your spouse both work, and share these expenses, perhaps you both pay into this account. I suggest contributing each month, and aiming for a month or two of cushion. You can include discretionary spending—which might range from groceries to entertainment—in here as well. This isn’t mandatory in the “budgeting” sense, but in the “things you pay each month” expense. In fact, this approach helps you keep tabs on your spending at a high level without having to nickel and dime each line item of your budget. If your cushion drops below that one-month level, you know that maybe you want to cut back. If you’re building up reserves in this account, you know you can loosen the belt a bit.

Irregular expense account

I suggest a separate savings account for big expenses that you know are coming (so they aren’t an emergency) but that aren’t the kind of thing you plan for each month. This includes fun things like family vacations or holiday shopping… as well as less fun things like property taxes or car insurance payments. By allocating money to this fund each month, you can avoid some of the pitfalls that come with irregular cash flow as an entrepreneur. It also protects your savings account, which is where most clients go for funds if they don’t have this type of irregular expense account set up.

A taxable investment account

Just like a retirement account, this isn’t a bank account, but I like to include it in the same conversation because it serves a purpose connected to your bank accounts. Namely, if you have a taxable investment account—like a brokerage account or something with your advisor—these investments don’t have the penalties usually associated with retirement account withdrawals (before 59.5 years old). They also tend to have a lower tax rate if you need to cash out investments, as they’re taxed as either short- or long-term capital gains versus as ordinary income. Yes, there are risks to selling out of investments, but this type of account can give you flexibility if you need cash. Maybe you never dip into it and you just let the money grow, but maybe you need it at some point. It’s always good to have that option. And if you open the account? That’s the first step towards funding it and giving yourself that additional flexibility.

Of course, these nine accounts are just a high level guide. Your spouse might want to add their own independent accounts to the mix taking your family (and business) tally well over 10. Or perhaps you’re disciplined enough to segment out a single bank account into clearly earmarked funds. The important thing is to find a system that works… then use it on purpose.